IIMS Journal of Management Science

Search

Search

Nishi Malhotra1 and Pankaj Kumar Baag1

and Pankaj Kumar Baag1

1 Indian Institute of Management Kozhikode, Kerala, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

UN has adopted poverty reduction and women empowerment as one of the sustainable development goals. Financial literacy is emerging as an essential tool to achieve financial inclusion through microfinance. Particularly with the advent of a pandemic such as COVID-19, the use of technology has increased manifold. Thus, the importance of financial literacy to ensure the sustainability of self-help groups has grown tremendously. There is a shortage of literature that measures the impact of financial literacy on the financial behavior of the members of self-help groups in India.

Moreover, research establishes that rote financial education leads to dormant knowledge with financial outcomes. Through the lens of Theory of Planned Behavior, the study demonstrates the mediating role of financial attitude and financial efficacy in explaining the relationship between financial knowledge and financial behavior. Peer influence leads to financial knowledge and behavior. But financial attitude is developed only through financial knowledge. Also, financial attitude enhances the impact of financial knowledge and peer influence on financial behavior. This study uses the partial least square structural equation modeling method for the data analysis, and the results establish that financial knowledge and attitude positively impact behavior. Financial attitude and efficacy mediate the relationship between financial knowledge and financial behavior. Thus, an individual’s emotional disposition should be considered while designing social intermediation initiatives. Also, social learning through peer influence can be extremely helpful in promoting sound financial habits.

Financial literacy, financial attitude, self-help groups, financial efficacy

Introduction

Globally 1.7 billion people are excluded from the financial system (Kunt, 2017), and these people lack access to physical collateral. Due to a lack of financial acumen, they use informal sources of credit, resulting in no credit history. The formal institutions do not have access to financial information about the creditworthiness of these micro borrowers. Due to this information asymmetry, formal financial institutions are wary of lending to these poor (Stiglitz, 1990). This information asymmetry leads to high transaction, monitoring, and screening costs. The financial exclusion due to the information asymmetry is termed credit market failure in finance and leads to under-allocation of finance to the poor. In this scenario, group lending based on social capital enables the financial inclusion of the poor. Thus, the self-help group bank linkage program (SBLP) launched by NABARD in 1999 is a unique landmark model that facilitates the financial inclusion of the poor.

Under Deen Dayal Upadhyay Antyodaya Yojana–National Rural Livelihood Mission, 5.96 crore rural Indian women are linked to 54.07 million self-help organizations. Various demand side issues such as lack of financial and institutional sustainability due to lack of financial literacy hamper the success of this SBLP. Self-help group members do not keep financial records, books of accounts, or meeting minutes, leading to a decrease in credit generation and thrift. United Nations’ sustainable development goals highlight the importance of financial inclusion and financial literacy in poverty reduction (Marcolin & Abraham, 2006). The literature attributes their financial exclusion to a lack of motivation. The studies show that insufficient financial knowledge promotes bad financial behavior. There is a need for an operational definition of financial literacy to operationalize the construct of financial knowledge through attitude building. This study mainly aims at analyzing the impact of financial literacy and peer influence on the financial behavior of the members of the group lending process. This study uses the theoretical lens of the Theory of Planned Behaviour (TPB) to develop a structural model to measure the impact of financial knowledge on financial behavior. The theory highlights the relevance of motivational intents and subjective attitudes in promoting desired behavior. According to the theory, subjective norms, financial attitudes, and societal factors affect micro borrowers’ financial behavior.

RQ: What is the role of financial literacy in enhancing credit creation and promoting thrift savings and timely repayment of loans through SHG Bank Linkage? What is the impact of Financial Literacy on Financial outcomes of SBLP?.

Literature Review

The rural finance system suffers from financial exclusion. As a result of the absence of collateral and knowledge asymmetry, most economically disadvantaged micro borrowers are excluded from the financial system. And they cannot process the financial data required to use these services. Emerging economies have realized the value of banking in fostering economic growth. Developing economies have accepted the UN Sustainable Development Goal 2030 to enhance financial inclusion and eliminate poverty. Money management has become more challenging as financial services and products have become more complicated. However, the lack of social intermediation prevents the marginalized poor from accessing financial services, jeopardizing universal banking. And financially illiterate persons experience increased debt levels due to a lack of financial abilities, leading to a vicious debt cycle (Cole & Shastry, 2008). Although experts disagree on the skills and abilities required, financial literacy has emerged as a significant factor impacting the universalization of banking and financial services. Financial literacy is knowledge, skills, confidence, and willingness to save money (Marcolin & Abraham, 2006). Remund (2010) defined financial literacy as a combination of conceptual and operational components. Taking cognizance of all the review studies undertaken to date, the author defined financial literacy as (a) knowledge of financial concepts, (b) ability to communicate financial concepts, (c) aptitude for managing personal finances, (d) skillset required to make appropriate financial concepts, and (e) confidence required to planning effectively. Globally, the scholars have identified the importance of financial knowledge, and literature emphasizes the importance of financial literacy (Braunstein et al., 2002).

Definitions and Concept of Financial Literacy

In the extant literature, the ability or aptitude for managing personal finance is the most critical factor impacting financial inclusion. Many researchers define financial literacy as the ability or aptitude to manage personal finances (Volpe et al., 1996). Financial literacy is characterized as managing cash and payment commitments and understanding essential financial and banking services, such as bank accounts and insurance products, using a holistic concept of inclusion and universal financial services (Emmons, 2005; Welch et al., 2002). Literacy in financial matters is the capacity to read, evaluate, manage, and communicate personal financial issues (Borden et al., 2008; Hogarth & Hilgert, 2002). Financial literacy is synonymous with financial knowledge (OECD, 2013). The OECD concentrated on three key aspects of financial literacy: financial knowledge, financial behavior, and financial attitude. Researchers have different opinions on financial literacy (Huston, 2010; Lusardi & Mitchell, 2011; Mandell & Klein, 2007).

Financial Knowledge

There is no comprehensive definition of financial literacy. Initially, financial literacy was defined as financial knowledge. Earlier, the financial knowledge based on cognitive financial concepts was called theoretical financial literacy understanding. According to the report, socio-demographic factors influence financial literacy for measuring financial literacy (Hira & Loibl, 2006) Compared to the previous study, this study also includes numeracy and consumer rights and responsibilities. This study adopts fluid as well as crystallized intelligence to measure financial literacy. As per Beal and Delpachitra (2003), their study designed a survey to measure financial literacy by understanding the critical basic financial concepts, financial markets and instruments, financial planning, financial analyses, and insurance and risk management tool. The study aimed to test the individual persons’ proficiency regarding basic financial concepts. Hogarth and Hilgert (2002), in their research, suggested an instrument to test the ability of individuals regarding personal finance. Financial knowledge comprises measures such as cash flow management, general credit management, savings, investment, mortgages, and other financial management topics. Income, income management, saving and investing, and spending and debt are all highlighted indicators of financial understanding (Malhotra & Baag, 2021).

Financial Attitude

Huston (2010) in his study argues that financial knowledge is not equal to financial literacy. As per the author, financial knowledge is an endogenous concept, and unless and until it results in financial self-efficacy, it will not lead to financial behavior. As per the author, financial literacy is a combination of financial literacy, financial attitude, and behavior. Financial attitude has not been discussed explicitly in the literature. Hung et al. (2009) in their research paper discussed financial knowledge as a broader concept that comprises financial education, skills, and abilities. Many tests used numeracy to measure financial literacy, a concept of crystallized intelligence. The author argues that financial attitude is distinct from capacity, skills, and abilities. Mandell and Klein (2009) in their research study highlight the paradox that financial education does not directly lead to financial literacy (Mandell, 2008). His research article propounds that financial education does not lead to financial literacy. He cites the difference in resources as the main reason behind the difference in outcomes of financial education. Also, JumpStart surveys highlighted that financial education might not lead to financial behavior. Mandell (2008) clarifies this issue by arguing that financial education gained through curriculum might be dormant, and individuals might not be able to use this education due to the lack of skills and abilities (Remund, 2010). His research study has highlighted the complexity of defining the concept of financial literacy. The scholar argues that financial literacy is defined as operationalized and conceptual financial literacy within the extant literature. This conceptual definition of literacy leads us to a hypothesis that:

H1:Financial knowledge has a positive impact on financial attitude.

Financial Behavior

Most studies state that financial education leads to financial literacy, which leads to financial conduct and contentment. The primary measures to promote savings, borrowing, and financial inclusion among micro borrowers are called financial behavior (Scheresberg, 2013). Their research study has mentioned three primary financial behaviors for financial well-being: high borrowing costs, precautionary savings and planning, and retirement. Menkhoff’s (2017) research paper mentions that financial literacy leads to financial behavior. Financial behavior comprises financial decisions such as borrowing and debt management, budgeting and planning behavior, saving and retirement saving, insurance and risk mitigation, remittance behavior, and bank account behavior (Bruhn et al., 2013). From the literature review, we hypothesize:

H2:Financial attitude leads to positive financial behavior.

H3:Financial knowledge has a positive impact on financial behavior.

H4:Financial attitude mediates the relationship between financial knowledge and financial behavior.

H5:Financial attitude mediates the relationship between financial behavior and peers’ influence.

Peer Influence

Peer influence on financial behavior has been a research topic for many empirical studies. Manski (1993) recognizes the impact of peer influence on social behavior, including information on social norms, social reactions, considerations for identity, and strategic complementarities (Benjamin et al., 2010). According to the literature, peer effects have a greater role in financial behavior in a group setting. Elison and Fudenberg refer to peer effect as a major factor that impacts financial behavior. Bernheim (1994) states that in a group, the peers imitate each other. Brown et al. (2008) emphasize the role of social capital and social interrelation in promoting financial behavior (Malhotra & Baag, 2021). From the synthesis of extant literature, we hypothesize

H6:Peer influence directly impacts the financial attitude of the members of the self-help group.

H7:Peer influence directly impacts the financial behavior of the members of the self-help group.

H8:Peer influence directly impacts the financial efficacy of the members of the self-help group.

H9:Peer influence directly impacts the financial knowledge of the members of the self-help group.

Self-efficacy

This study operationalizes the self-efficacy of the individual borrower to transform financial education into financial literacy. Mandell and Klein (2007) argue that motivation plays a significant role in transforming financial education or knowledge into financial behavior. Lewin (1938) in his theory has furthered the perspective on motivation. Vroom (1964) explains the underlying motivations behind human behavior in instrumentality, expectancy, and valence or utility. This theory, through the instrumentality, defines the difference in performance or outcomes and through instrumentality or valence, that is, through reward and utility. Burnet (1965) in his book argues that financial literacy is not simply knowing about financial concepts but also includes other personal and psychological dispositions, including achievement orientation, making choices, and pursuing leisure pursuits, to name a few. Repository propagates that individual makes sense of information using skills and technology, resources, and contextual knowledge to make informed decisions (Malhotra & Baag, 2021).

H10:Financial efficacy leads to a positive financial attitude.

H11:Financial efficacy leads to positive financial behavior.

H12:Financial knowledge has a positive effect on self-efficacy.

H13:Financial efficacy mediates the relationship between financial knowledge and financial behavior.

H14:Financial efficacy mediates the relationship between peer effect and financial behavior.

H15:Financial efficacy mediates the relationship between financial knowledge and financial attitude.

H16:Financial attitude mediates the relationship between financial efficacy and financial attitude.

H17:Financial attitude and financial efficacy serially mediates the relationship between financial knowledge and financial behavior.

There is a lack of empirical studies on financial literacy as a broader concept that includes financial knowledge, behavior, and attitude (Huston, 2010). Our study aims to empirically validate the structural relationship between financial knowledge, attitude, efficacy, peer influence, and behavior. It is the first-ever study to validate the structural model in India’s context of group lending.

Theoretical Lens

Through extant literature, the issue of dormant learning without effective results in terms of behavior is discussed through the theoretical lens of Expectancy Theory (Vroom, 1964), also called the force model and the utility model (Samuelson, 1967). The outcome of the performance of the task, as per Locke (1990) is dependent on the efficacy of individual goals and objectives. The literature also mentions the subject of financial literacy through the lens of the Expectancy Theory. In this study, we have used the TPB. The TPB (Ajzen, 1991) states that mere behavior controls and knowledge are not enough for the desired behavior change. But motivational intents, that is, an individual’s motivational factors, peer influence, financial efficacy, and attitudes, play an essential role. Within the TPB (Ajzen, 1991), we discuss the impact of financial knowledge on behavior given the financial attitude, financial efficacy, and peer influence.

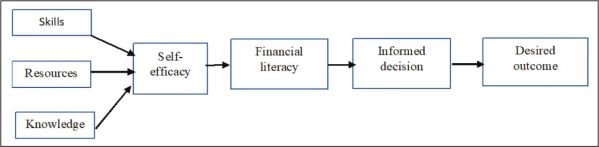

Structural Model

In this study, we intend to study the mediating impact of financial attitude and financial self-efficacy on financial behavior. Figure 1 describes the two-pronged mediation analysis.

Figure 1.Conceptual Model.

Research Methodology

As the problem is exploratory, we have used the PLS-SEM method. The justification for using the PLS-SEM model is the lean sample size and multiple structural relationships (Hair et al., 2019; Hair et al., 2021; Sarstedt et al., 2017). In our study, multiple independent variables have a structural relationship with the dependent variable. Thus, the use of regression models is not possible. Hence, to test the hypothesis in this study, we have used the PLS-SEM method (Hair et al., 2019). The PLS-SEM method is justified due to the lack of distributional assumption and mediation and moderator analyses (Nitzl et al., 2016). Due to this, we have used the PLS-SEM method of data analysis (Sarstedt et al., 2022). The structural model for our study is given in Figure 2.

Figure 2.Hypothesized Structural Equation Model.

.jpg/10_1177_0976030X221128711-fig2(1)__700x365.jpg)

Design of the Research Instrument

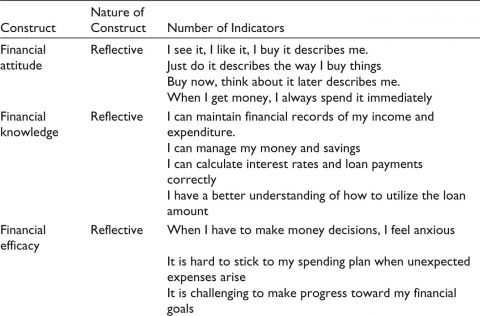

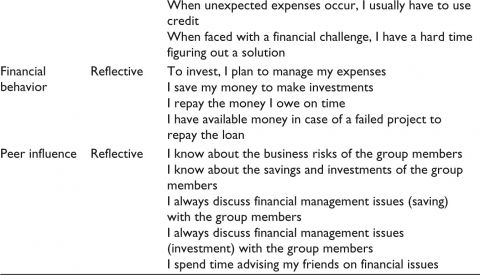

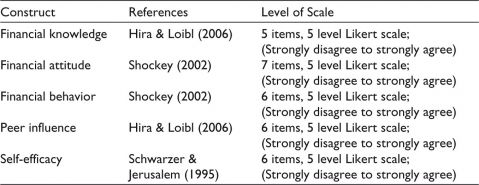

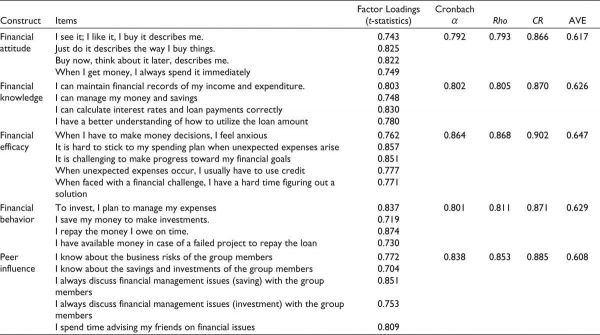

Previous researchers who have studied financial literacy (Hilgert & Hogarth, 2003; Lusardi & Mitchell, 2011; Mandell, 2008; OECD, 2013) have used the questionnaire survey as the tool for the collection of data. The scales have been adopted from the extant literature and modified for study. Table 1 provides a prototype or copy of the questionnaire. The items in the questionnaire were randomized with multiple sets to prevent bias in data collection. The following sources, as mentioned in Table 2, have been used for obtaining the scales for measuring the relevant constructs scales for measuring the relevant constructs.

Table 1.Questionnaire and Nature of Constructs.

Table 2.Scale Items and Literature Reference.

Sample Size

PLS-SEM is helpful when the small sample size and the model contain multiple components (Hair et al., 2017). The sample size was decided based on an apriori study (i.e., before the survey) and a post hoc investigation. The sample size was determined using G power a priori, post hoc assessments. We calculated a sample size of 252 from this test, nearly four times the recommended sample size of 74. As a result, we used a sample size of 252 for our analysis. For the pilot study, 10% of the 250 approximately 40 participants were utilized for data analysis (Agita Putri, 1998; Connelly, 2008; Hertzog, 2003).

Data Collection

In this study, the data were collected using the primary questionnaire. Questionnaires contain questions in the domain of 5 latent constructs, that is, financial knowledge, financial attitude, financial behavior, financial efficacy, and peer influence. The questions to collect data measured the constructs on a Likert scale of 1 = “Strongly disagree” to 5 = “Strongly agree.” Data were collected from the self-help group members from September to October 2021. The primary data were collected using excel mode and computer-aided technology at the SPADE SHG in Purulia and Man Bazaar center in Kolkata, India. SPADE is an NGO and is a member of the West Bengal self-help group promotional forum, a state-level network of self-help group promoting institutions (SHPIs) in West Bengal since 2001. A pilot study was conducted with 25 women self-help group members in Kolkata, India, using the gatekeeper (Connelly, 2008; Hertzog, 2018) to ensure that the responses were accurate. Further in this study, we have used reflective constructs with indicators.

Data Analysis

This experiment was analyzed using SmartPLS software. Since this is an experimental study, we have used the Partial Least Squares Structural Equational Modelling (Hair et al., 2011; Hair et al., 2017; Hair et al., 2019; Sharma et al., 2021). A two-step procedure was used to analyze the study’s conceptual framework: The first stage of the study validated the quality of the scale using the measurement model. The hypothesis was tested using the non-parametric bootstrapping technique in the second stage (Wetzels, 2009). Our model includes one-dimensional structures (i.e., financial attitude, financial knowledge, financial efficacy, peer control, and financial behavior). There were reflective indicators (Jarvis et al., 2003) for financial knowledge, financial attitude, financial efficacy, peer control, and financial behavior. As a result, this study presents a composite measurement model with a reflecting design (Henseler, 2018). We constructed a measuring model based on the buildings (Henseler, 2017). Financial attitude and efficacy were negatively worded and transformed accordingly using SPSS. The output showed that the six factors with an eigenvalue greater than 1, with the first factor explaining approximately 29.45% of the total variance, which is way below the 50% threshold, and thus there is no threat of Common Method Variance (CMV) in the study.

Normality Test

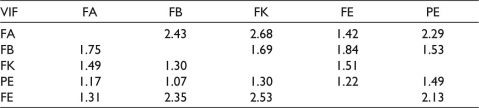

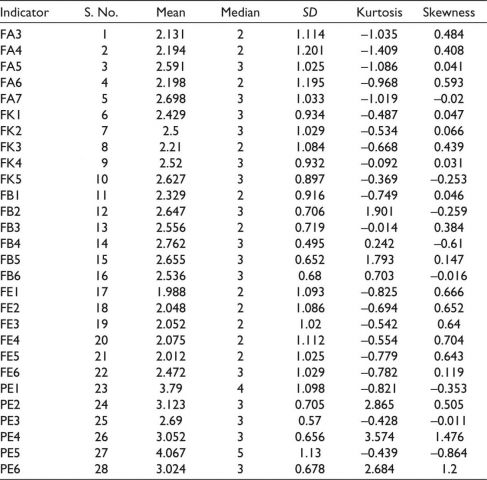

The lack of a normal distribution is the primary reason for using the PLS-SEM model (Hair et al., 2012). However, this is not sufficient justification. The non-normal data assumption can impact the PLS-SEM results in some instances. The confidence intervals for skewness are managed through bias-corrected, corrected, and accelerated (BCa) bootstrapping. We used the univariate and multivariate analyses of the skewness and kurtosis to evaluate the distributional assumptions. These results are given in the Appendix of the study. Most of the Kurtosis and Skewness in the univariate analysis are between +/–2 (George & Mallery, 2010; Mardia, 1970). The presence of outliers was determined using online software (Zhang & Yuan, 2018) to determine the multivariate normality of the data using the Mardia test. The skewness and kurtosis obtained from the Mardia web power platform suggested that the data were multivariate non-normal. Mardia’s multivariate skewness (β = 4.23, p < .001) and Mardia’s multivariate kurtosis is (β = 46.88, p < .001). Thus, multivariate kurtosis and skewness are way beyond the threshold limit, that is, the measure of skewness >+/–1 and skewness >+/–20, and data are non-normal. Nonnormality in the data is the main reason for using the PLS-SEM for analysis (Hair et al., 2019; Mardia, 1970; Zhang & Yuan, 2018). The full collinearity test suggested by Kock (2015) (as mentioned in Table 3 that VIF values ranging from 1.070 to 2.68 for all the latent constructs below the threshold limit of 3.3 suggest that Common Method Bias (CMB) is not the problem for the current study. The results of VIF are given in Table 3.

Table 3.Full Collinearity Test VIF.

Note: FK: Financial knowledge, FE: Financial efficacy, FA: Financial attitude, FB: Financial behavior, PE: Peer effect.

Measurement Model

The measurement model for the study is in Figure 3.

Figure 3.Measurement Model.

.jpg/10_1177_0976030X221128711-fig3(1)__700x375.jpg)

The first step in the measurement model is to examine the indicator loadings. Loadings above 0.708 are recommended, thus providing acceptable indicator reliability. The second step is assessing internal consistency reliability. Reliability between 0.7 and 0.95 is acceptable. Though the values above 0.95 are not acceptable (Diamantopoulos et al., 2012). Cronbach alpha and composite reliability, the indicator of internal consistency reliability, have a value of above 0.7 and below 0.95 (Nunnally & Bernstein, 1994). The results of measurement model are given in Table 4.

Table 4.Measurement Model.

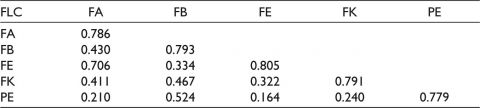

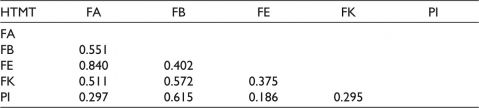

Similarly, Rho has values above 0.7 (Dijkstra & Henseler, 2015) establishing the internal consistency reliability. The third step in the reflective measurement model assessment addresses the convergent validity of each construct measure. The metric for assessing this convergent validity is the average variance extracted (AVE) for all the constructs. The AVE exceeded the threshold of 0.5 (Bagozzi & Yi, 1998). The fourth step is to assess the discriminant validity, which is the extent to which construct is empirically distinct from constructs in the structural model. Heterotrait–Monotrait Ratio of Correlation (HTMT) values were used to validate the discriminant validity (Fornell & Larcker, 1981). The results of Fornell and Larcker criteria are given in Table 5. The HTMT values were less than 0.85 and below 0.90; hence there were no issues regarding the discriminant validity (Henseler et al., 2015) in the model. The results of HTMT are given in Table 6.

Table 5.Fornell and Larcker Criteria.

Table 6. Measurement Model: Heterotrait–Monotrait Ratio (HTMT)–Discriminant Validity.

Structural Model

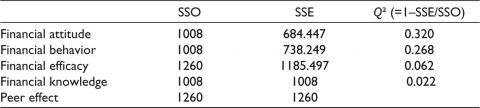

We used the proportion of variance explained to assess the accuracy of the model’s prediction. The results show R2 for the dependent variable. According to the blindfolding process used in the PLS, the stone Neisser Q2 value was used to examine the predictive relevance (Chin, 2010; Hair et al., 2009). Multicollinearity was measured using the Variance Information Factor, and all values were less than the recommended benchmark of 3.33 (Hair et al., 2019). From the model analysis, it becomes apparent that the model has no multicollinearity issue. The R2 value represents and explains the variance of the dependent concept. The model explains 54% of the variance in the financial attitude of a model and 44.3% of the variance in the financial behavior. The model explains 11.2% of the variance in financial efficacy. However, the R2 for financial knowledge is low at 5.7%. R2 values are high to moderate (below 0.75), 0.540 for financial attitude, and 0.443 for financial behavior. It is moderate to low (below 0.5), 0.112 for financial efficacy, and 0.057 for financial knowledge (Hair et al., 2011; Hair et al., 2014; Shumeli, 2016). Thus, in our study, the variation explained is adequate for analysis.

Assessment of Structural Model

Table 4 includes the evaluation of the path coefficients and their significance level using the t-value (Hair et al., 2021; Wetzels et al., 2019). Bootstrapping (10,000 sub-sample) provides t – a value and confidence interval that allows the evaluation of the significance of the statistical relationship (Roldan & Sanchez-Franco, 2012). The results of the tests are shown in Table 8.

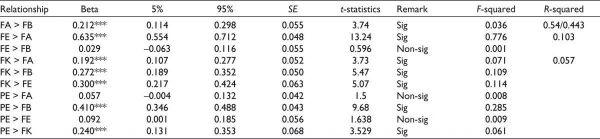

H2 :(Financial attitude – Financial behavior) Financial attitude has significant impact on financial behavior ((β1 = 0.212, p < .000, t-value = 3.84).

H10:(Financial efficacy – Financial attitude) Financial efficacy has significant impact on financial attitude with (β2 = 0.635, p < .000 and t-value = 13.33).

H11:(Financial efficacy – Financial behavior) Financial efficacy has insignificant impact on financial behavior with (β3 = 0.029, p < .000, t-value = 0.530).

H1:(Financial knowledge – Financial attitude) Financial knowledge has a significant impact on financial attitude, in support of the hypothesis (β3 = 0.192, p < .000, t = 3.753).

Figure 4.Structural Model.

.jpg/10_1177_0976030X221128711-fig4(1)__700x368.jpg)

Table 7.Q Square Predict.

Table 8.Direct Effect.

Note: *** 5% significance level.

There is a (Financial knowledge – Financial behavior) significant and positive influence of financial knowledge on behavior supporting H3 (β4 = 0.272, p < .000, t = 5.434). The relationship between financial knowledge and financial efficacy is significant; (H12 Financial knowledge – Financial efficacy) (β5 = 0.30; p < .000, t = 4.844). Finally, there is no significant relationship between peer effect and financial attitude (H6 Peer effect – Financial attitude) rejecting the (β7 = 0.057, p > .000, t = 1.38). Peer effect positively impacts financial behavior (H7 Peer effect – Financial behavior) (β6 = 0.410, p < .000, t = 9.572), and the impact is significant. Peer effect has no significant impact on financial efficacy (H8 Peer effect – Financial efficacy) at a 5% level of significance (β7 = 0.092, p < .000, t = 1.638), and peer effect has a significant impact on financial knowledge (H9: Peer effect – Financial knowledge) (β9 = 0.240, p < .000, t = 3.529). We used the size of f 2 to quantify the significant effects. The f 2 values are above the cut-off value of 0.02 for all construct relationships except between financial efficacy and financial behavior and peer effect and financial attitude and peer effect and financial efficacy. Specifically, there is a medium effect (values between 0.15 and 0.35) between peer effect and financial behavior. And there is a large effect between financial efficacy and financial attitude. And there is a less-than-average effect between financial efficacy and financial behavior and between peer effect and financial attitude and peer effect and financial efficacy. We also assessed the model by examining the dependent variables’ cross-validated redundancy index (Q2). Values above 0 suggest that the model shows predictive relevance (Hair et al., 2017). The results of Q square predict are given in Table 7.

Direct Effect

While designing this research, the authors have taken care of parsimony and brevity in line with Occam’s razor. The research model is theoretically positioned in the literature on financial intermediation.

Mediation Analysis

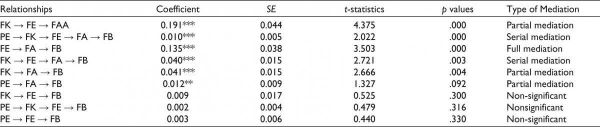

As per Ajzen’s (2017) theory of reasoned action, the financial attitude mediates the impact of financial knowledge on financial behavior. In the context of the SBLP, micro borrowers can access finance through their social capital. For the estimation of the mediation effect, we have used the percentile bootstrapping method (Aguirre-Urreta & Ronkko, 2018). The results for mediation analysis are given in Table 9.

Table 9.Indirect Effect.

Note: ** 10% significance level and *** 5% significance level.

In this model, the mediating effect of financial efficacy between financial knowledge and financial attitude (H15: Financial knowledge – Financial efficacy – Financial attitude) is significant; (β1 = 0.191; t = 4.375; p < .000). The mediating effect of financial efficacy between the peer effect and financial behavior is insignificant (H14: Peer effect – Financial efficacy – Financial behavior), (2 = 0.003; t = 0.440; p > .330). The mediating effect of financial efficacy between financial knowledge and financial behavior is insignificant; (H13: Financial knowledge – Financial efficacy – Financial behavior) (β3 = 0.009; t = 0.525; p < .300). The mediating effect of financial attitude between financial knowledge and financial behavior is significant (H4: Financial knowledge – Financial attitude – Financial behavior) (β5 = 0.041; t = 2.666; p < .004). The mediation analysis result indicates a partial complementary mediation (abc, “the product of the indirect effect ab and the direct effect c,” is positive (Zhao et al., 2010). However, the impact of financial attitude between peer effect and financial behavior is non-significant (H5: Peer effect – Financial attitude – Financial behavior) (β6 = 0.012; t = 1.327; p < .092) is non-significant (Menon et al., 2021; Nitzl et al., 2016; Rasoolimanesh et al., 2021; Zhao et al., 2010). The mediating effect of financial attitude between financial efficacy and financial behavior is significant (H16: Financial efficacy – Financial attitude – Financial behavior) (β7 = 0.135; t = 3.503; p < .000). Also, the mediating effect of financial attitude between financial efficacy and financial behavior is full mediation as the indirect effect is significant and the direct effect of financial efficacy on financial behavior is not significant. The serial mediation between financial knowledge and financial behavior through financial attitude and financial efficacy is significant (β = 0.041; t = 2.666; p < .003). And the serial mediation effect between the peer effect on financial behavior through financial attitude, financial efficacy, and financial knowledge is significant given (β7 = 0.010; t = 2.022; p = .000). Also, the serial mediation effect between peer effect on financial behavior through financial knowledge and financial efficacy is insignificant (β8 = 0.002; t = 0.479; p = .316).

Moderation Analysis

In this study, we propose “peer influence” as a moderator to test the moderating effect. We argue that “peer influence” will moderate all the hypothesized relationships so that the impact of financial knowledge would be greater in the presence of peer influence. To illustrate the different approaches for generating the interaction data and data treatment, we draw on a simple mediation model of financial knowledge impacting financial behavior through financial attitude (Angela et al., 2009; Mpaata et al., 2010; Nano, 2015; Potrich et al., 2016; Xiao et al., 2010). Drawing on the literature, we consider the peer effect as a moderator variable that impacts the relationship between financial knowledge and financial behavior. The results of the moderation analysis are given in Figure 5.

Figure 5.Results of Moderation Analysis.

.jpg/10_1177_0976030X221128711-fig5(1)__724x416.jpg)

The results of the moderation analysis of the relationship between financial knowledge and financial behavior, moderated through the peer effect, are mentioned in Table 10.

Table 10.Results of Moderating Impact of Peer Influence on the Effect of Financial Knowledge on Financial Behavior.

.jpg/10_1177_0976030X221128711-table11(1)__480x57.jpg)

Note: *** 5% significance level.

This section presents the results of the simple moderation analysis performed. These models considered financial behavior as the dependent variable, financial knowledge as the independent variable, and the peer effect as the moderating variable. A BCa bootstrapped CI based on 10,000 samples was used to calculate the models’ confidence intervals. From the analysis of the results, a significant difference between the groups is inferred from the p values, less than 0.000. The PLS-SEM moderation analysis results are shown in Table 10.

Conclusion

This article aims to empirically validate the various structural relationships present in the conceptual model of financial literacy through the theoretical lens of the TPB. The study shows that social learning can help members of a group to make sound financial decisions. The members get together in a social setting, share information, discuss financial decisions, and make decisions suitable for their finances. So, the peer effect leads to social learning and good financial habits. In a social setting, a person’s financial attitude, how he feels about money, and his financial efficacy or belief in his abilities lead to good financial habits. Financial knowledge is vital in promoting financial attitude and thus efficacy among the group members. An individual’s financial attitude magnifies the impact of peer influence and financial knowledge on the financial behavior of the members of the joint liability group. Financial attitude is the source of financial efficacy among the community members, and without a financial attitude, individuals lack efficacy, which leads to poor financial habits. Peer influence moderates the impact of financial knowledge on financial behavior. Social intermediation can be helpful in building a financial attitude to boost self-efficacy. Through initial handholding, NGOs and SHPIs can design programs to develop financial attitudes among community members. There is a lack of research theory in the domain of the impact of social norms and background on the financial behavior of the person. Further, research can be conducted to study the impact of other indicators such as subjective norms in studying the impact of subjective norms on the financial behavior of the person.

Limitations of the Study

This study only covers only women’s self-help groups. Studying mixed-gender self-help groups in other parts of the country is also possible. Further studies can be conducted to empirically validate the other scales of financial literacy with more indicators. Research can be conducted to empirically test the differences in the impact of financial literacy on groups mentored by the SHPIs and not promoted by the SHPIs. Lastly, further studies can also include other variables such as financial socialization and the use of digital technology.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

ORCID iD

Nishi Malhotra  https://orcid.org/0000-0003-0000-3749

https://orcid.org/0000-0003-0000-3749

Appendix

Aguirre-Urreta, M. I., & Ronkko, M. (2018). Statistical inference with PLSc using bootstrap confidence. MIS Quarterly, 42, 1001–1020.

Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behavior. Prentice-Hall.

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Process, 50, 179–211.

Angela, A. H., Andrew, M. P., & Joanne, K. Y. (2009). Defining and measuring financial literacy [Working Papers WR-708]. RAND Corporation.

Bagozzi, R., & Yi, Y. (1988) On the evaluation of structural equation models. Journal of the Academy of Marketing Sciences, 16, 74–94. http://dx.doi.org/10.1007/BF02723327

Beal, D. J., & Delpachitra, S. B. (2003, March). Financial literacy among australian university students. Economic Papers, The Economic Society of Australia, 22(1), 65–78.

Benjamin, D. J., Choi, J. J., & Strickland, A. J. (2010). Social identity and preferences. The American Economic Review, 100(4), 1913–1928. http://www.jstor.org/stable/27871281

Bernheim, B. D. (1994). A theory of conformity. Journal of political Economy, 102, 841–877. http://dx.doi.org/10.1086/261957

Borden, L. M., Lee, S. A., Serido, J., & Collins, D. (2008). Changing college students’ financial knowledge, attitudes, and behavior through seminar participation. Journal of Family and Economic Issues, 29(1), 23–40. https://doi.org/10.1007/s10834-007-9087-2

Braunstein, S. F., & Welch, C. (2002, November). Financial literacy: An overview of practice, research, and policy. Federal Reserve Bulletin, Board of Governors of the Federal Reserve System (U.S.), 88, 445–457.

Brown, B. B., Bakken, J. P., Ameringer, S. W., & Mahon, S. D. (2008). A comprehensive conceptualization of the peer influence process in adolescence. In M. J. Prinstein & K. A. Dodge (Eds), Understanding peer influence in children and adolescents (pp. 17–44). The Guilford Press.

Bruhn, M., de Souza Leão, L., Legovini, A., Marchetti, R., & Zia, B. (2013) The impact of high school financial education: Experimental evidence from Brazil [World Bank Policy Research Working Paper, 6723]. World Bank.

Burnet, M. (1965). ABC of financial illiteracy. United Nation.

Chin, W. W. (2010) How to write up and report PLS analyses. In V. V. Esposito, W. W. Chin, J. Henseler & H. Wang (Eds), Handbook of partial least squares: Concepts, methods and applications (pp. 655–690). Springer.

Cole, S., & Shastry, G. (2008). If you are so smart, why aren’t you rich The effects of education, financial literacy and cognitive ability on financial market participation. https://afiweb.afi.es/eo/FinancialLiteracy.pdf

Demirguc-Kunt, A., Klapper, L., & Singer, D. (2017). Financial inclusion and inclusive growth : A review of recent empirical evidence [Policy Research Working Paper No. 8040]. World Bank. https://openknowledge.worldbank.org/handle/10986/26479

Diamantopoulos, A., Sarstedt, M., Fuchs, C., Wilczynski, P., Kaiser, S. (2012). Guidelines for choosing between multi-item and single-item scales for construct measurement: a predictive validity perspective. Journal of the Academy of Marketing Science, 40, 434–449. https://doi.org/10.1007/s11747-011-0300-3

Dijkstra, T. K., & Henseler, J. (2015) Consistent partial least squares path modeling. MIS Quarterly, 39, 297–316.

Emmons, R. A. (2005). Emotion and religion. In R. F. Paloutzian & C. L. Park (Eds), Handbook of the psychology of religion and spirituality (pp. 235–252). The Guilford Press.

Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18, 382–388.

George, D., & Mallery, M. (2010). SPSS for Windows step by step: A simple guide and reference, 17.0 Update (10th ed.). Pearson.

Hair, J., Black, W. C., Babin, B. J., & Anderson, R. E. (2009). Multivariate data analysis: A global perspective (7th ed). Prentice Hall Print.

Hair, J., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling (PLS-SEM) (2nd ed.). SAGE Publications.

Hair, J., Ringle, C., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19, 139–151.

Hair, J., Sarstedt, M., Ringle, C., & Mena, J. (2012). An assessment of the use of partial least squares structural equation modeling in marketing research. Journal of the Academy of Marketing Science, 40, 414–433. https://doi.org/10.1007/s11747-011-0261-6

Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modelling. SAGE Publications.

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31, 2–24. https://doi.org/10.1108/EBR-11-2018-0203

Henseler, J. (2017). Bridging design and behavioral research with variance-based structural equation modeling. Journal of Advertising, 46(1), 178–192. https://doi.org/10.1080/00913367.2017

Henseler, J. (2018) Partial least squares path modeling: Quo vadis Quality & Quantity, 52, 1–8. https://doi.org/10.1007/s11135-018-0689-6

Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43, 115–135. https://doi.org/10.1007/s11747-014-0403-8

Hertzog, C., Hülür, G., Gerstorf, D., & Pearman, A. M. (2018). Is subjective memory change in old age based on accurate monitoring of age-related memory change Evidence from two longitudinal studies. Psychology and Aging, 33(2), 273–287. https://doi.org/10.1037/pag0000232

Hertzog, N. (2003). Impact of gifted programs from the students’ perspectives. Gifted Child Quarterly, 47, 131–143. https://doi.org/10.1177/001698620304700204

Hilgert, M. A., & Hogarth, J. M. (2003). Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin, 309–322. https://www.federalreserve.gov/pubs/bulletin/2003/0703lead.pdf

Hira, T. K., & Loibl, C. (2006). A workplace and gender-related perspective on financial planning information sources and knowledge outcomes. Financial Services Review, 15, 21.

Hogarth, J., & Hilgert, M. A. (2002). Financial literacy and family and consumer sciences. Journal of Family and Consumer Sciences: From Research to Practice, 94(1), 15–28.

Hung, A. A., Parker, A. M., & Yoong, J. (2009). Defining and measuring financial literacy [Working Paper 708]. RAND Corporation. https://www.rand.org/content/dam/rand/pubs/working_papers/2009/RAND_WR708.pdf

Huston, S. J. (2010). Measuring financial literacy. Journal of Consumer Affairs, 44(2), 296–316. https://doi.org/10.1111/j.1745-6606.2010.01170.x

Huston, S. J. (2010). Measuring financial literacy. The Journal of Consumer Affairs, 44(2), 296–316.

Jarvis, C. B., MacKenzie, S. B., & Podsakoff, P. (2003). A critical review of construct indicators and measurement model specification in marketing and consumer research. Journal of Consumer Research, 30, 199–218.

Kaiser, T., & Menkhoff, L. (2017). Does financial education impact financial literacy and financial behavior, and if so, when Oxford University Press. https://openknowledge.worldbank.org/handle/10986/31469

Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration, 11(4), 1–10.

Lewin, K. (1938). Expectancy Theory. In The conceptual representation and the measurement of psychological forces (pp. 15–24). Duke University Press.

Locke, E. A. (1990). A theory of goal setting and task performance.

Lusardi, A., & Mitchell, O. S. (2011). Financial literacy around the world: An overview [NBER Working Papers No 17107]. National Bureau of Economic Research.

Mandell, L., & Klein, L. S. (2009). The impact of financial literacy education on subsequent financial behavior. Journal of Financial Counseling and Planning, 20(1), 15–24.

Manski, C. F. (1993). Identification of endogenous social effects: The reflection problem. The Review of Economic Studies, 60(3), 531–542. https://doi.org/10.2307/2298123

Marcolin, S., & Abraham, A. (2006). Financial literacy research: Current literature and future opportunities. https://ro.uow.edu.au/cgi/viewcontent.cgiarticle=1233&context= commpapers

Mardia, K. V. (1970). Measures of multivariate skewness and kurtosis with applications. Biometrika, 57, 519–530.

Malhotra, N., & Baag, P. (2021). Process views of peer mechanism in joint group lending through the theoretical lens of agency Theory: A systematic review of literature. IIMS Journal of Management Science, 12(3), 144–162.

Mandell, L. (2008). The financial literacy of Young American adults. JumpStart.

Mandell, L., & Klein, L. S. (2007). Motivation and financial literacy. Financial Services Review, 16, 105–116.

Menon, M. A., Ramayah, T., Cheah, J-H., Ting, H., Chuah, F., & Cham, T. H. (2021). PLS-SEM statistical programs: A review. Journal of Applied Structural Equation Modeling, 1(1), 1–14.

Mpaata, E., Koskei, N., & Saina, E. (2010). Financial literacy and saving behavior among micro and small business enterprise owners in Kampala, Uganda: The moderating role of social influence. Journal of Economics, Finance and Accounting Studies, 2(1), 22–34.

Nitzl, C., Roldan, J. L., & Capeda-Carrion, G. (2016). Mediation analysis in PLS-SEM Path modeling: Helping researchers discuss more sophisticated models. Industrial Management and Data Systems, 116(9), 1849–1864.

Nunnally, J. C., & Bernstein, I. H. (1994) The assessment of reliability. Psychometric Theory, 3, 248–292.

OECD. (2013). How’ life Measuring well-being. https://www.oecd.org/sdd/3013071e.pdf

Potrich, A. C. G., Vieira, K. M., & Mendes-Da-Silva, W. (2016). Development of a financial literacy model for university students. Management Research Review, 39(3), 356–376.

Putri, A. (1998). What sample size is enough in internet survey research Interpersonal Computing and Technology: An Electronic Journal for 21st Century, 6(3–4), 1–10.

Rasoolimanesh, S. M., Wang, M., Roldan, J., & Kunasekaran, P. (2021). Are we in right path for mediation analysis Reviewing the literature and proposing robust guidelines. Journal of Hospitality and Tourism Management, 8(1), 395–405.

Remund, D. L. (2010). Financial literacy explicated: The case for a career definition in an increasingly complex economy. Journal of Consumer Affairs, 44(2), 276–295.

Roldán, J. L., & Sánchez-Franco, M. J. (2012). Variance-based structural equation modeling: Guidelines for using partial least squares in information systems research. https://doi.org/10.4018/978-1-4666-0179-6.ch010

Sarstedt, M., Radomir, L., Moisescu, O. I., & Ringle, C. M. (2022). Latent class analysis in PLS-SEM: A review and recommendations for future applications. Journal of Business Research, 138, 398–407.

Samuelson, P. (1967). Economics. McGraw-Hill Book Co.

Schwarzer, R., & Jerusalem, M. (1995). Generalized self-efficacy scale. In J. Weinman, S. Wright & M. Johnston (Eds), Measures in health psychology: A user’s portfolio. Causal and control beliefs (pp. 35–37). NFER-NELSON.

Shockey, S. S. (2002). Low-wealth adults’ financial literacy, money management behaviors and associated factors, including critical thinking. Ohio University.

Sharma, A., Dwivedi, Y., Arya, V., & Siddiqui, M. Q. (2021). Does SMS advertising still have relevance to increase consumer purchase intention A hybrid PLS-SEM-neural network modelling approach. Computers in Human Behavior, 124. https://doi.org/106919.10.1016/j.chb.2021.106919

Shmueli, G., Ray, S., Velasquez Estrada, J., & Chatla, S. B. (2016). The elephant in the room: Evaluating the predictive performance of PLS models. Journal of Business Research, 69, 4552–4564. https://doi.org/10.1016/j.jbusres.2016.03.049

Stiglitz, J. (1990). Peer monitoring and credit markets. The World Bank Economic Review, 4, 351–366. http://dx.doi.org/10.1093/wber/4.3.351

Volpe, R. P., Chen, H., & Pavlicko, J. J. (1996). Personal Investment Literacy Among College Students. Financial Practice and Education. https://citeseerx.ist.psu.edu/viewdoc/downloaddoi=10.1.1.476.6325&rep=rep1&type=pdf

Vroom, V. H. (1964). Work and motivation. John Wiley & Sons.

Welch, R. M., & Graham, R. D. (2002). Breeding crops for enhanced micronutrient content. Plant and Soil, 245, 205–214. https://doi.org/10.1023/A:1020668100330

Wetzels, M., Odekerken-Schroder, G., & Oppen, C. Van. (2009). Using PLS path modeling for assessing hierarchical construct models: Guidelines and empirical illustration. MIS Quarterly, 33, 177–195.

Xiao, J. J., Serid, J., & Shim, S. (2010). Financial Education, Financial Knowledge and Risky Credit Behavior of College Students [NFI Working Papers 2010-WP-05]. Indiana State University, Scott College of Business, Networks Financial Institute.

Zhang, Z., & Yuan, K-H. (2018). Practical statistical power analysis using web power and R. ISDSA Press.

Zhao, X., Lynch, J. G., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. The Journal of Consumer Research, 37(2), 197–206.